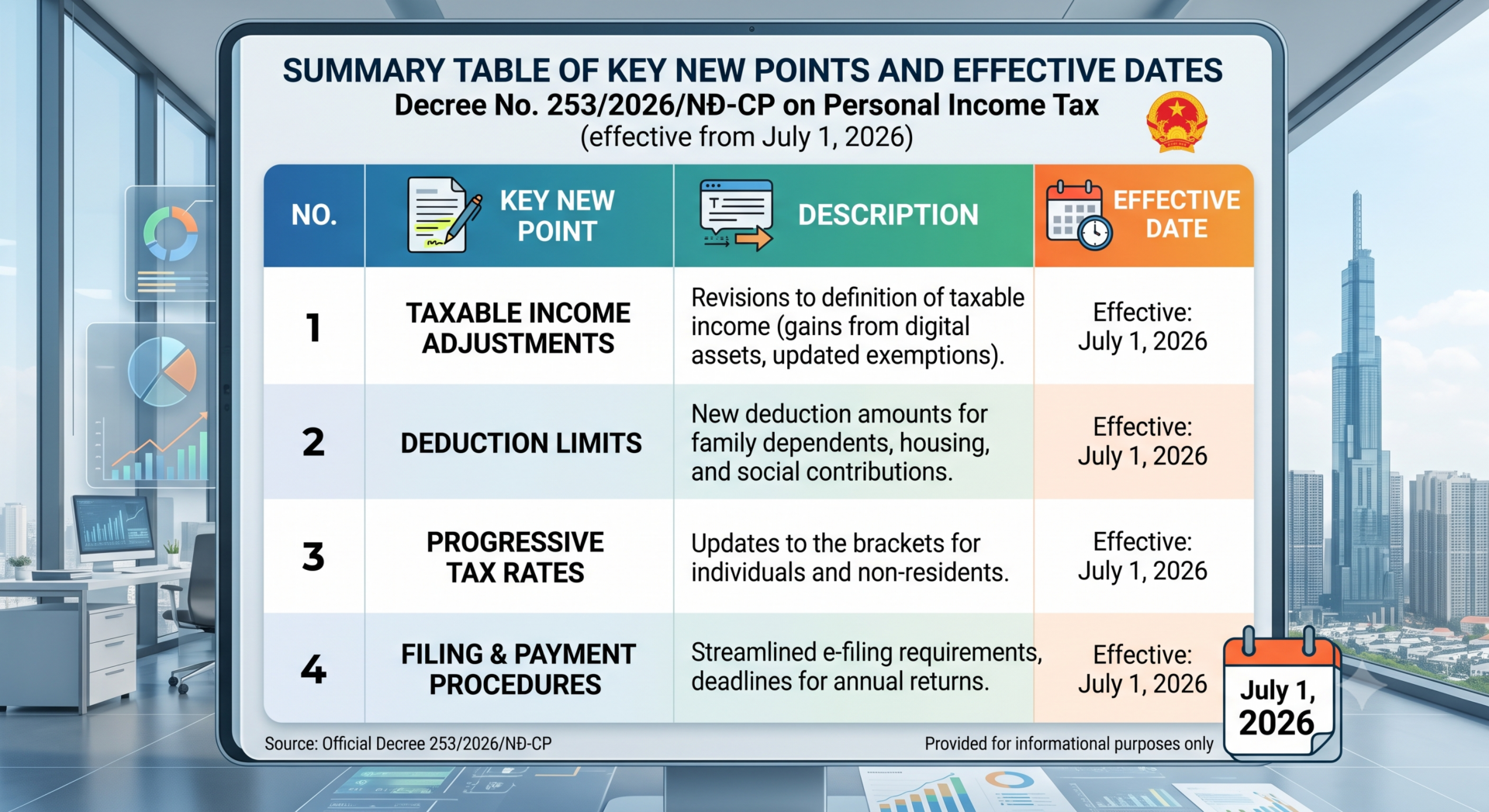

SUMMARY OF KEY NEW POINTS AND EFFECTIVE DATES of DECREE No. 253/2026/NĐ-CP on Personal Income Tax (Effective from July 1, 2026)

The important new points from Decree No. 253/2026/NĐ-CP and the specific implementation timelines for each group of regulations to help you easily track and comply:

- Summary Table of Key New Points and Effective Dates

| No. | Regulation Group / Content | Key New Points to Note | Effective / Application Date |

| 1 | General Validity of the Decree | Replaces the entirety of Decree No. 65/2013/NĐ-CP and older amended documents regarding Personal Income Tax (PIT). | From July 1, 2026 |

| 2 | Income from Salaries, Wages & Business of Resident Individuals | Comprehensively applies the new regulations, tax brackets, and calculation methods under this Decree. | Applied fully for the 2026 tax year. (The initial months of 2026 declared under the old law will be adjusted during the 2026 annual tax finalization). |

| 3 | Mid-shift / Lunch Meal Allowances | Raises the maximum amount excluded from taxable income to VND 1.2 million/person/month. | From July 1, 2026 |

| 4 | Deductions for Medical and Education Expenses | Adds two completely new deductions to taxable income:

– In-country medical examination and treatment expenses (under the Health Insurance catalog): maximum VND 23 million/year.

– In-country education and training expenses (from kindergarten to university, vocational): maximum VND 24 million/year. |

Calculated from the 2026 tax year (when performing annual tax finalization). |

| 5 | Voluntary, Supplementary Pension & Life Insurance | Deductible contribution limits when calculating tax are increased to a maximum of VND 3 million/month (including both the business’s contribution and the employee’s self-payment). | Contribution fees from January 1, 2026 are eligible for this deduction limit; insurance companies will withhold 10% at the time of maturity. |

| 6 | E-commerce & Digital Platform Business | E-commerce platform owners (with online ordering and payment functions) are responsible for withholding, declaring, and paying taxes on behalf of individual sellers on the platform. | From July 1, 2026 |

| 7 | Addition of New Taxable Assets | Income from transferring: carbon credits, auctioned license plates (5% tax rate) for income exceeding VND 20 million per transfer, and digital assets/encrypted assets (0.1% tax rate). | From July 1, 2026 |

| 8 | Incentives for Tech Personnel & Startups | – 5-year PIT exemption for salaries of high-tech and high-quality digital industry personnel (AI, semiconductors, chips, etc.).

– Tax exemption on capital investment income into startups/venture capital funds; tax exemption on salaries of experts supporting startups. |

From July 1, 2026 (calculated continuously from the month the tax-exempt income arises). |

| 9 | Tax Exemption for Open-Ended Fund Certificates | PIT exemption when transferring open-ended fund certificates, provided the individual has held them for at least 2 consecutive years from the date of purchase. | Transfers executed from July 1, 2026 (applies to certificates purchased before July 1, 2026 as well). |

| 10 | Tax Reduction on Investment Fund Dividends | 50% PIT reduction on dividends distributed from securities investment funds and real estate investment funds. | Within 5 years: From July 1, 2026, to the end of June 30, 2031. |

| 11 | Changes to Tax Thresholds (Prizes, Copyrights, etc.) | Raises the taxable income threshold to the portion exceeding VND 20 million per occurrence (previously VND 10 million) for prizes, copyrights, franchises, inheritances, and gifts. | From July 1, 2026 |

- Three Major Timelines Requiring Special Attention

To avoid errors when performing tax obligations in 2026, it is necessary to clearly distinguish between the following 3 implementation milestones:

- Transition Period (From January 1, 2026, to before July 1, 2026):

- Taxpayers declare and pay monthly/quarterly taxes according to old regulations.

- There is no need to re-submit tax declaration files for these months/quarters; instead, corrections and offsets for discrepancies will be made directly when filing the 2026 annual tax finalization dossier.

- Application Period for New Regulations on Salaries, Wages, and Family Deductions (Full Year 2026):

- Although the Decree officially takes effect in July, the tax calculation policies for income from salaries, wages, and business of resident individuals are applied to the entire 2026 tax year.

- This ensures taxpayers benefit from the new deductions (medical, education) calculated against their income for the full year of 2026.

- Effective Milestone from July 1, 2026:

- The new lunch/mid-shift meal allowance level (VND 1.2 million) applies immediately.

- The new VND 20 million tax threshold applies immediately to irregular incomes arising from this date onward (prizes, inheritances, etc.).

- The 5-year tax exemption period for high-tech personnel or the 50% tax reduction for investment funds begins counting from this date.